Tax-Free(ish) Tips and Overtime: Breaking Down OBBBA’s Newest Perks

In this article, we're going to talk about the no-tax-on-tips and no-tax-on-overtime provisions that were enacted as part of the One Big Beautiful Bill Act (Public Law 119‑21 AKA OBBBA). These deductions have been widely received as positives for the industries they affect. Workers in jobs where they traditionally receive tips, and employees who regularly earn overtime, can be big winners under these new rules. But how do they actually work? In this article, we’re going to cover the basics of each deduction and dive into some of the details.

Overview of OBBBA. OBBBA was enacted on July 4th, 2025. The bill came out of a need to ensure that taxpayers could continue receiving the benefits of the 2017 Tax Cuts and Jobs Act as its sunset approached. Not only did OBBBA extend taxpayer friendly provisions beyond 2025, but it also created several new deductions—including the no tax on tips and no tax on overtime deductions.

The bill introduced many tax changes, including the two we’re talking about here. Some of the changes are permanent, while others—such as the no tax on tips and no tax on overtime deductions—are temporary. The “no tax on...” deductions only apply to tax years 2025 through 2028.

What Counts as Qualified Overtime & Tips

Let’s talk about what qualifies as qualified tips and qualified overtime.

Tips

To qualify for the deduction, a tip must be:

· Voluntary

· Not negotiated

· Determined by the customer

Mandatory service charges do not qualify. For example, if a restaurant automatically adds gratuity for parties of eight or more, the automatic gratuity portion does not count toward the no tax on tips deduction.

Planning tip: Restaurants and other employers that use mandatory service charges may want to consider moving away from them so employees can receive this deduction.

Additionally, only occupations that customarily receive tips (as of 12/31/2024) qualify. Examples include waitstaff, bartenders, rideshare drivers, hair stylists, caddies, and similar roles.

IRS guidance on qualifying tipped occupations can be found here:

https://www.irs.gov/newsroom/treasury-irs-issue-guidance-listing-occupations-where-workers-customarily-and-regularly-receive-tips-under-the-one-big-beautiful-bill

Overtime

Only overtime required under the Fair Labor Standards Act (FLSA) qualifies for the overtime deduction. Specifically, the premium portion of overtime—meaning the extra 0.5× in “time and a half”—is the deductible amount.

This means:

State only overtime rules (e.g., California daily overtime) do not qualify

Voluntary overtime bonuses do not qualify

Example:

An employee earns $20/hr and works 50 hours. Under FLSA, they must be paid $30/hr for 10 overtime hours. The deductible portion is the premium only: 10 hours × $10 premium = $100 deductible amount.

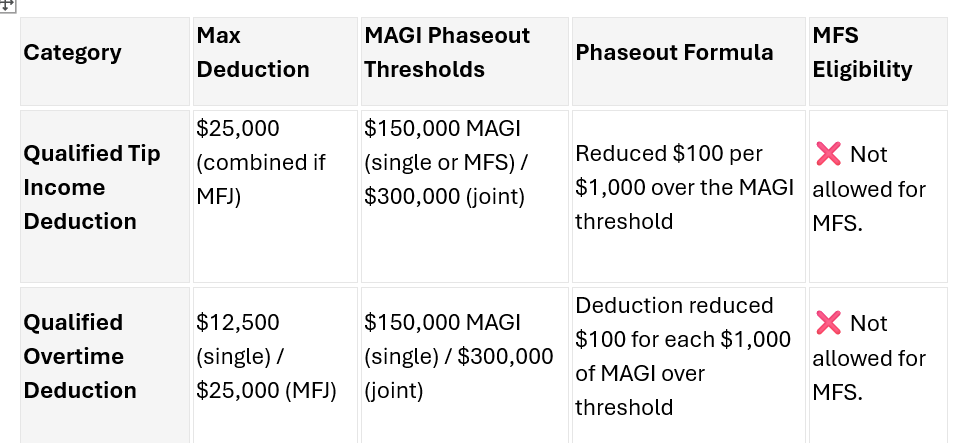

Deduction and MAGI Limits/Phaseouts

Colloquially, each of these is known as a “no tax on…” deduction. But do they truly result in tax free treatment? No. Both the tips and overtime deductions reduce income taxes, not payroll taxes (FICA taxes still apply). Additionally, each deduction has a cap.

Each deduction has its own deduction limits and phaseout thresholds. Below is a table summarizing these amounts.

Employers Reporting Tips and Overtime to Employees

Tips

Good news: new W‑2 and 1099 forms will be available starting in 2026 to help employers report this information. You might notice that’s a year after the deductions begin. For 2025, employers are not required to report qualified tips on the W‑2 due to IRS transition relief.

To report qualified tips, employers may use:

Box 14 of Form W‑2 or

A separate statement

Observation: While employers can use Box 14, it is generally better practice to use a separate statement or provide the information via an online portal.

Employees can rely on various methods outlined in Notice 2025-69 to determine their qualified tips, including:

Tips reported in Box 7 of Form W‑2

Employer provided supplemental statements

Qualified tips reported in Box 14

Personal pay stubs or tip logs

These tips must be reported as income to the employer or via Form 4137.

Overtime

Employers should report qualified overtime premiums in:

Box 14 of Form W‑2 or

A separate statement

Just like qualified tips, a separate statement is generally preferred.

Note: Some states have enacted their own no tax on overtime deductions and may require separate state specific reporting.

Each of the new “no tax on...” deductions will be claimed on Schedule 1-A.

Need Help?

If you have questions about how the no tax on tips or no tax on overtime rules apply to your situation—or if you’d like help planning around these new deductions—please reach out to us. We’re here to walk you through the details, review your specific circumstances, and make sure you’re getting the full benefit of the new provisions. Please email:

Professional Disclaimer

This article is for informational and educational purposes only.